- Published on

Islamic Contract – Bay’ al-Murābahah: Supplier Requirement in Murābahah Transactions

Q1: What is the role of the supplier in a murābahah transaction?

Answer:

In a murābahah transaction, the supplier is the party from whom the Islamic bank or seller purchases the asset before reselling it to the customer at a disclosed markup price.

The supplier plays an important role because:

Q2: What is the AAOIFI position regarding the supplier in murābahah?

Answer:

According to AAOIFI Shariah Standard No. 8 (Para 2/2/3):

Bay‘ al-‘īnah refers to a sale and buy-back arrangement that may be used as a legal stratagem to obtain cash financing resembling an interest-based loan.

AAOIFI adopts this requirement to ensure:

Q3: What is the BNM position regarding the supplier?

Answer:

The Bank Negara Malaysia (BNM) Policy Document on Murābahah does not specifically require the supplier to be a third party.

However, according to Paragraph 23:

Comparison Notes: AAOIFI vs BNM on Supplier Requirement

AAOIFI Position

Case Study 1: Permissible Third-Party Supplier Arrangement

A customer requests an Islamic bank to finance the purchase of factory equipment.

The bank:

Case Study 2: Potential Bay‘ al-‘Īnah Concern

A customer sells his own asset to an Islamic bank and immediately repurchases the same asset through murābahah at a higher deferred price.

Analysis

Notes: Important Principles Regarding Suppliers in Murābahah

AAOIFI Emphasis

Murābahah must involve:

Q1: What is the role of the supplier in a murābahah transaction?

Answer:

In a murābahah transaction, the supplier is the party from whom the Islamic bank or seller purchases the asset before reselling it to the customer at a disclosed markup price.

The supplier plays an important role because:

- the murābahah transaction must involve a genuine purchase and ownership transfer; and

- the Islamic bank must own the asset before reselling it to the customer.

Q2: What is the AAOIFI position regarding the supplier in murābahah?

Answer:

According to AAOIFI Shariah Standard No. 8 (Para 2/2/3):

- the supplier should be a third party; and

- the arrangement should not lead to bay‘ al-‘īnah.

Bay‘ al-‘īnah refers to a sale and buy-back arrangement that may be used as a legal stratagem to obtain cash financing resembling an interest-based loan.

AAOIFI adopts this requirement to ensure:

- the transaction represents a genuine trade;

- there is actual transfer of ownership and risk; and

- the murābahah structure is not used to disguise ribā-based financing.

Q3: What is the BNM position regarding the supplier?

Answer:

The Bank Negara Malaysia (BNM) Policy Document on Murābahah does not specifically require the supplier to be a third party.

However, according to Paragraph 23:

- ownership transfer must be genuine; and

- it must be supported by proper and sufficient documentation.

- evidencing genuine ownership transfer;

- ensuring actual sale transactions occur; and

- preventing fictitious or paper-based transactions.

Comparison Notes: AAOIFI vs BNM on Supplier Requirement

AAOIFI Position

- Supplier should be an independent third party.

- Arrangement must not result in bay‘ al-‘īnah.

- Adopts stricter safeguards against legal stratagems.

- Emphasises genuine commercial transactions.

- Does not expressly require a third-party supplier.

- Focuses on genuine ownership transfer.

- Requires sufficient documentation to evidence the transaction.

- Emphasises operational substance and documentary compliance.

Case Study 1: Permissible Third-Party Supplier Arrangement

A customer requests an Islamic bank to finance the purchase of factory equipment.

The bank:

- purchases the equipment from an independent supplier;

- obtains ownership and supporting documents; and

- resells the equipment to the customer through murābahah.

- Supplier is a genuine third party.

- Ownership transfer occurs properly.

- The transaction satisfies AAOIFI and BNM requirements.

Case Study 2: Potential Bay‘ al-‘Īnah Concern

A customer sells his own asset to an Islamic bank and immediately repurchases the same asset through murābahah at a higher deferred price.

Analysis

- The arrangement may resemble bay‘ al-‘īnah.

- AAOIFI generally discourages such structures.

- Concern exists that the transaction merely disguises cash financing with profit increments similar to ribā.

- the focus would be on whether genuine ownership transfer and documentation exist;

- however, Shariah governance mechanisms would still examine whether the arrangement is substantively compliant.

Notes: Important Principles Regarding Suppliers in Murābahah

AAOIFI Emphasis

- Third-party supplier preferred.

- Avoidance of bay‘ al-‘īnah.

- Stronger anti-ribā safeguards.

- Genuine ownership transfer.

- Proper legal documentation.

- Evidence of actual commercial transaction.

Murābahah must involve:

- real asset ownership;

- genuine transfer of risk; and

- actual sale transactions rather than disguised lending arrangements.

- Published on

Islamic Contract – Bay’ al-Istisnā‘: Definition and Nature of Manufacturing Sale

Q1: What is Bay’ al-Istisnā‘?

Answer:

The word istisnā‘ is derived from the Arabic verb istaṣna‘a, which means:

“to request the manufacture of an asset.”

Technically, Bay’ al-Istisnā‘ (hereinafter, istisnā‘) refers to:

a contractual agreement with a manufacturer to produce or construct an asset with specified descriptions at a pre-determined price to be delivered on an agreed future date.

In an istisnā‘ contract:

Q2: What are the main characteristics of an istisnā‘ contract?

Answer:

The main characteristics of istisnā‘ are as follows:

Manufacturing or Construction Basis

The contract involves:

The asset must be clearly specified, including:

The manufactured asset is delivered at a future agreed date.

Pre-Determined Price

The contract price must be agreed upon at the beginning of the contract.

Flexibility of Payment

Payment may be:

Q3: What types of assets are commonly subject to istisnā‘?

Answer:

Istisnā‘ is commonly used for assets requiring manufacturing or construction, such as:

Case Study 1: Construction of a House

Ahmad enters into an istisnā‘ contract with a construction company to build a house.

Contract Details

Case Study 2: Manufacturing of Industrial Machinery

A factory owner orders specialised machinery from a manufacturer through istisnā‘ financing.

Contract Details

Notes: Important Features of Istisnā‘

Nature of Contract

Q1: What is Bay’ al-Istisnā‘?

Answer:

The word istisnā‘ is derived from the Arabic verb istaṣna‘a, which means:

“to request the manufacture of an asset.”

Technically, Bay’ al-Istisnā‘ (hereinafter, istisnā‘) refers to:

a contractual agreement with a manufacturer to produce or construct an asset with specified descriptions at a pre-determined price to be delivered on an agreed future date.

In an istisnā‘ contract:

- one party requests the manufacture or construction of an asset;

- the manufacturer agrees to produce it according to agreed specifications; and

- delivery takes place in the future.

Q2: What are the main characteristics of an istisnā‘ contract?

Answer:

The main characteristics of istisnā‘ are as follows:

Manufacturing or Construction Basis

The contract involves:

- manufacturing;

- construction; or

- production of an asset.

The asset must be clearly specified, including:

- quantity;

- quality;

- design;

- measurements; and

- other relevant specifications.

The manufactured asset is delivered at a future agreed date.

Pre-Determined Price

The contract price must be agreed upon at the beginning of the contract.

Flexibility of Payment

Payment may be:

- made upfront;

- deferred; or

- paid progressively according to stages of completion.

Q3: What types of assets are commonly subject to istisnā‘?

Answer:

Istisnā‘ is commonly used for assets requiring manufacturing or construction, such as:

- houses;

- buildings;

- ships;

- aircraft;

- roads;

- machinery;

- furniture; and

- customised products.

- Islamic project financing;

- infrastructure development; and

- construction financing.

Case Study 1: Construction of a House

Ahmad enters into an istisnā‘ contract with a construction company to build a house.

Contract Details

- Type of asset: Double-storey house

- Contract price: RM500,000

- Construction period: 18 months

- Payment structure:

- RM100,000 upfront;

- RM200,000 during construction;

- RM200,000 upon completion.

- size;

- number of rooms;

- building materials; and

- design layout.

- The house does not yet exist at the time of contract.

- The manufacturer (contractor) agrees to construct it.

- Delivery will occur in the future.

- Price and specifications are predetermined.

Case Study 2: Manufacturing of Industrial Machinery

A factory owner orders specialised machinery from a manufacturer through istisnā‘ financing.

Contract Details

- Machinery price: RM1,200,000

- Manufacturing period: 12 months

- Payment arrangement:

- 30% upon signing;

- 40% during production;

- 30% upon delivery.

- machine capacity;

- technical features;

- materials used; and

- performance requirements.

- The machinery will be manufactured according to specifications.

- Delivery occurs in the future.

- Payment is structured progressively.

- The contract satisfies the requirements of istisnā‘.

Notes: Important Features of Istisnā‘

Nature of Contract

- Manufacturing or construction contract.

- Asset may not yet exist at contract formation.

- Clear specifications.

- Agreed price.

- Agreed delivery timeline.

- Upfront payment allowed.

- Deferred payment allowed.

- Progressive payment allowed.

- Construction projects.

- Infrastructure financing.

- Manufacturing industries.

- Islamic project financing.

- Published on

Islamic Contract – Bay’ al-Murābahah: Late Payment Charges in Murābahah Transactions

Q1: What are late payment charges in murābahah financing?

Answer:

Late payment charges refer to charges imposed on customers who fail to make payment within the agreed payment period in a murābahah contract.

In Islamic finance, late payment charges are carefully regulated to ensure that they:

Q2: What is the AAOIFI position regarding late payment charges?

Answer:

According to AAOIFI Shariah Standard No. 8 (Para 5/6):

Q3: What is the BNM position regarding late payment charges?

Answer:

According to the Bank Negara Malaysia (BNM) Policy Document on Murābahah (Para 19.1):

Meaning of Gharamah

Comparison Notes: AAOIFI vs BNM on Late Payment Charges

AAOIFI Position

Case Study 1: AAOIFI Approach on Late Payment

An Islamic bank provides murābahah financing for equipment.

Figures

“In the event of late payment, the customer undertakes to contribute 1% of overdue instalments for charitable purposes.”

Calculation

Case Study 2: BNM Approach on Late Payment

An Islamic bank grants home financing through murābahah.

Figures

Ta‘wīd (Compensation)

RM12,000 \times 1\% \times \frac{4}{12}

12000 \times 1% \times \frac{4}{12} = 40

Ta‘wīd payable = RM40

Additional gharamah may also be imposed according to regulatory guidelines.

Analysis

Notes: Important Principles Regarding Late Payment Charges

AAOIFI Emphasis

Late payment charges in Islamic finance must:

Q1: What are late payment charges in murābahah financing?

Answer:

Late payment charges refer to charges imposed on customers who fail to make payment within the agreed payment period in a murābahah contract.

In Islamic finance, late payment charges are carefully regulated to ensure that they:

- do not amount to ribā (interest); and

- are imposed only for legitimate Shariah purposes such as compensation or deterrence against intentional delay.

Q2: What is the AAOIFI position regarding late payment charges?

Answer:

According to AAOIFI Shariah Standard No. 8 (Para 5/6):

- the murābahah contract may include an undertaking by the customer to pay an amount of money or percentage of the debt upon late payment;

- however, the amount collected must be donated to charitable causes.

- the Islamic bank cannot treat the penalty amount as profit or income;

- the purpose is mainly to discourage deliberate default by customers.

- benefiting financially from late payment resembles ribā;

- therefore, any collected penalty should not enrich the bank.

Q3: What is the BNM position regarding late payment charges?

Answer:

According to the Bank Negara Malaysia (BNM) Policy Document on Murābahah (Para 19.1):

- the murābahah contract may include a clause imposing late payment charges;

- these charges may consist of:

- gharamah (penalty); and

- ta‘wīd (compensation).

Meaning of Gharamah

- Penalty imposed to deter late payment.

- Usually channelled for charitable purposes and not recognised as bank profit.

- Compensation for actual loss suffered by the bank due to delayed payment.

- May be recognised as income to the extent of actual losses incurred.

- Shariah compliance;

- operational practicality; and

- financial discipline in Islamic banking.

Comparison Notes: AAOIFI vs BNM on Late Payment Charges

AAOIFI Position

- Late payment undertaking allowed.

- Amount collected must be donated to charity.

- Bank cannot profit from customer’s delay.

- Stronger precaution against ribā.

- Late payment charges expressly allowed.

- Includes:

- gharamah (penalty); and

- ta‘wīd (compensation).

- Charges subject to regulatory limits.

- Bank may recover actual losses through ta‘wīd.

Case Study 1: AAOIFI Approach on Late Payment

An Islamic bank provides murābahah financing for equipment.

Figures

- Murābahah selling price: RM120,000

- Monthly instalment: RM2,000

- Customer delays payment for 3 months.

“In the event of late payment, the customer undertakes to contribute 1% of overdue instalments for charitable purposes.”

Calculation

- Overdue amount = RM6,000

- 1% late payment amount = RM60

- cannot be recognised as bank profit;

- must be channelled to charity.

- Purpose is deterrence, not profit-making.

- This arrangement complies with AAOIFI standards.

Case Study 2: BNM Approach on Late Payment

An Islamic bank grants home financing through murābahah.

Figures

- Murābahah selling price: RM500,000

- Monthly instalment: RM3,000

- Customer delays payment for 4 months.

- Total overdue amount = RM12,000

- ta‘wīd rate = 1% per annum;

- gharamah imposed according to BNM guidelines.

Ta‘wīd (Compensation)

RM12,000 \times 1\% \times \frac{4}{12}

12000 \times 1% \times \frac{4}{12} = 40

Ta‘wīd payable = RM40

Additional gharamah may also be imposed according to regulatory guidelines.

Analysis

- Ta‘wīd compensates the bank for actual losses caused by delayed payment.

- Gharamah functions as a deterrent penalty.

- The arrangement complies with BNM requirements.

Notes: Important Principles Regarding Late Payment Charges

AAOIFI Emphasis

- Penalties allowed only as deterrence.

- Amount collected must go to charity.

- Bank cannot profit from delay.

- Allows both:

- ta‘wīd (compensation); and

- gharamah (penalty).

- Charges regulated by authorities.

- Bank may recover actual losses.

Late payment charges in Islamic finance must:

- avoid ribā;

- prevent injustice;

- encourage payment discipline; and

- remain within Shariah-approved limits.

- Published on

Islamic Contract – Bay’ al-Murābahah: Ibrā’ (Rebate) in Murābahah Transactions

Q1: What is Ibrā’ in Islamic finance?

Answer:

Ibrā’ refers to a rebate, waiver, or remission granted by the seller or Islamic bank to the purchaser by reducing part of the outstanding payment obligation.

In murābahah financing, ibra’ commonly occurs when:

Q2: Why is Ibrā’ important in murābahah financing?

Answer:

Ibrā’ is important because murābahah financing usually involves deferred payment over a long period.

When customers:

Q3: What is the AAOIFI position regarding Ibrā’?

Answer:

According to AAOIFI Shariah Standard No. 8 (Para 5/9):

Q4: What is the BNM position regarding Ibrā’?

Answer:

According to the Bank Negara Malaysia (BNM) Policy Document on Murābahah (Para 18.2):

Comparison Notes: AAOIFI vs BNM on Ibrā’

AAOIFI Position

Case Study 1: AAOIFI Approach on Ibrā’

An Islamic bank finances machinery through murābahah.

Figures

The bank voluntarily grants:

Case Study 2: BNM Approach on Ibrā’

An Islamic bank provides home financing through murābahah.

Figures

“The customer shall be entitled to ibra’ for early settlement based on the bank’s rebate formula.”

After 10 years:

Notes: Important Principles Regarding Ibrā’

AAOIFI Emphasis

Ibrā’ represents:

Q1: What is Ibrā’ in Islamic finance?

Answer:

Ibrā’ refers to a rebate, waiver, or remission granted by the seller or Islamic bank to the purchaser by reducing part of the outstanding payment obligation.

In murābahah financing, ibra’ commonly occurs when:

- the customer settles the financing earlier than scheduled; or

- the bank voluntarily grants a discount on the outstanding balance.

Q2: Why is Ibrā’ important in murābahah financing?

Answer:

Ibrā’ is important because murābahah financing usually involves deferred payment over a long period.

When customers:

- make early settlement; or

- complete payment before maturity,

- unearned profit; or

- part of the remaining sale price.

- the bank receives payment earlier than expected; and

- the bank no longer bears financing risk for the remaining period.

Q3: What is the AAOIFI position regarding Ibrā’?

Answer:

According to AAOIFI Shariah Standard No. 8 (Para 5/9):

- ibra’ cannot be stipulated as part of the murābahah contract.

- the bank cannot contractually promise a rebate in advance;

- ibra’ must remain a voluntary act by the seller.

- making ibra’ contractually binding may resemble interest recalculation in conventional loans.

- the rebate should be discretionary and not pre-agreed within the contract itself.

Q4: What is the BNM position regarding Ibrā’?

Answer:

According to the Bank Negara Malaysia (BNM) Policy Document on Murābahah (Para 18.2):

- ibra’ must be included as part of the contract if required by the regulator.

- Islamic financial institutions are generally required to specify ibra’ clauses in financing agreements.

- promote transparency;

- protect customers;

- standardise early settlement calculations; and

- ensure fairness in Islamic financing practices.

Comparison Notes: AAOIFI vs BNM on Ibrā’

AAOIFI Position

- Ibrā’ cannot be part of the murābahah contract.

- Rebate must remain voluntary.

- Concerned that contractual rebate resembles interest adjustment.

- Emphasises discretionary benevolence.

- Ibrā’ clause must be included if required by regulation.

- Rebate calculation becomes transparent and predictable.

- Protects customers in early settlement situations.

- Widely applied in Malaysian Islamic banking practice.

Case Study 1: AAOIFI Approach on Ibrā’

An Islamic bank finances machinery through murābahah.

Figures

- Cost price: RM100,000

- Profit margin: RM20,000

- Murābahah selling price: RM120,000

- Payment period: 5 years

The bank voluntarily grants:

- RM8,000 rebate (ibrā’) on the remaining balance.

- The rebate was not pre-promised in the contract.

- The bank granted it voluntarily.

- This complies with AAOIFI standards.

Case Study 2: BNM Approach on Ibrā’

An Islamic bank provides home financing through murābahah.

Figures

- House purchase cost: RM300,000

- Profit margin: RM90,000

- Murābahah selling price: RM390,000

- Financing tenure: 20 years

“The customer shall be entitled to ibra’ for early settlement based on the bank’s rebate formula.”

After 10 years:

- outstanding balance = RM220,000

- bank grants RM25,000 ibra’

- customer pays final settlement amount = RM195,000

- Ibrā’ was expressly included in the contract.

- Rebate calculation was transparent and predetermined.

- This complies with BNM regulatory requirements.

Notes: Important Principles Regarding Ibrā’

AAOIFI Emphasis

- Ibrā’ should remain voluntary.

- Cannot be contractually stipulated.

- Avoids resemblance to conventional interest adjustments.

- Ibrā’ clause included for transparency.

- Regulatory protection for customers.

- Standardised industry practice.

Ibrā’ represents:

- fairness;

- benevolence; and

- equitable treatment in deferred payment transactions.

- Published on

Islamic Contract – Bay’ al-Murābahah: Meaning of “Absorbing the Takaful Cost”

Q1: What does “absorbing the takaful cost” mean in murābahah?

Answer:

“Absorbing the takaful cost” means bearing or paying the takaful contribution associated with the asset.

In the context of murābahah:

“the purchaser may absorb the takaful cost before entering into the murābahah contract,”

it means:

Example 1: Seller Absorbs the Takaful Cost (AAOIFI Approach)

An Islamic bank purchases machinery for murābahah financing.

Figures

Here:

RM200,000 + RM5,000 = RM205,000 acquisition cost

The customer then pays:

RM225,000 = RM205,000 cost + RM20,000 profit

Key Point

The takaful cost becomes part of the murābahah selling price because the bank paid it first.

Example 2: Purchaser Absorbs the Takaful Cost (BNM Approach)

A customer applies for Islamic vehicle financing.

Figures

Before the murābahah contract:

The purchaser “absorbs” the takaful cost because:

Simple Difference Between the Two Approaches

Seller Absorbs Takaful Cost

Q1: What does “absorbing the takaful cost” mean in murābahah?

Answer:

“Absorbing the takaful cost” means bearing or paying the takaful contribution associated with the asset.

In the context of murābahah:

- the takaful cost may either be borne by the seller (Islamic bank); or

- paid directly by the purchaser (customer), depending on the contractual arrangement.

“the purchaser may absorb the takaful cost before entering into the murābahah contract,”

it means:

- the customer agrees to pay the takaful contribution separately before the murābahah sale contract is executed.

Example 1: Seller Absorbs the Takaful Cost (AAOIFI Approach)

An Islamic bank purchases machinery for murābahah financing.

Figures

- Cost of machinery: RM200,000

- Takaful contribution paid by bank: RM5,000

- Total acquisition cost: RM205,000

- Profit margin: RM20,000

- Murābahah selling price: RM225,000

Here:

- the bank initially bears (“absorbs”) the takaful cost of RM5,000;

- the bank includes it as part of the acquisition cost.

RM200,000 + RM5,000 = RM205,000 acquisition cost

The customer then pays:

RM225,000 = RM205,000 cost + RM20,000 profit

Key Point

The takaful cost becomes part of the murābahah selling price because the bank paid it first.

Example 2: Purchaser Absorbs the Takaful Cost (BNM Approach)

A customer applies for Islamic vehicle financing.

Figures

- Vehicle price: RM100,000

- Takaful contribution: RM3,000

- Bank’s profit margin: RM15,000

- Murābahah selling price: RM115,000

Before the murābahah contract:

- the customer separately agrees to pay the RM3,000 takaful contribution directly.

- the bank’s acquisition cost remains RM100,000;

- the murābahah selling price becomes RM115,000 only.

- RM3,000 takaful contribution; and

- RM115,000 murābahah price.

- Murābahah price = RM115,000

- Separate takaful payment = RM3,000

- Total overall payment = RM118,000

The purchaser “absorbs” the takaful cost because:

- the customer personally bears and pays the takaful expense instead of the bank including it in the murābahah cost.

Simple Difference Between the Two Approaches

Seller Absorbs Takaful Cost

- Bank pays takaful first.

- Takaful included in murābahah cost.

- Customer indirectly pays through instalments.

- Customer pays takaful separately.

- Takaful excluded from murābahah cost.

- Murābahah selling price becomes lower.

- Published on

Islamic Contract – Bay’ al-Murābahah: Takaful Coverage for Asset Under Seller’s Possession

Q1: What is the purpose of takaful coverage in a murābahah transaction?

Answer:

In a murābahah transaction, the seller or Islamic bank may obtain takaful coverage for the asset while it remains under the seller’s ownership and possession before being sold to the purchaser.

The purpose of takaful is to:

This reflects the Shariah principle:

“Risk accompanies ownership.”

Since the seller owns the asset before resale, the seller bears the associated risks during that ownership period.

Q2: What is the AAOIFI position regarding takaful cost?

Answer:

According to AAOIFI Shariah Standard No. 8 (Paras 3/2/6–3/2/7):

This means the seller initially bears the takaful responsibility because the seller still owns the asset before transferring ownership to the purchaser.

⸻

Q3: What is the BNM position regarding takaful cost?

Answer:

According to the Bank Negara Malaysia (BNM) Policy Document on Murābahah (Para 17.5):

This allows:

However, the arrangement must be:

Comparison Notes: AAOIFI vs BNM on Takaful Cost

AAOIFI Position

BNM Position

Case Study 1: AAOIFI Approach with Figures

An Islamic bank purchases industrial machinery for a customer under a murābahah arrangement.

Transaction Details

The bank obtains takaful coverage while the machinery remains under its ownership before reselling it to the customer.

Analysis

Case Study 2: BNM Approach with Figures

A customer applies for murābahah vehicle financing from an Islamic bank.

Transaction Details

Before the murābahah contract is concluded, the customer separately agrees to pay the RM3,000 takaful contribution.

Analysis

Notes: Important Principles Regarding Takaful in Murābahah

AAOIFI Emphasis

BNM Emphasis

Common Shariah Principle

The party bearing ownership risk should generally bear the corresponding liabilities and responsibilities associated with the asset until ownership is transferred.

Q1: What is the purpose of takaful coverage in a murābahah transaction?

Answer:

In a murābahah transaction, the seller or Islamic bank may obtain takaful coverage for the asset while it remains under the seller’s ownership and possession before being sold to the purchaser.

The purpose of takaful is to:

- protect the asset against damage or loss;

- manage ownership risks borne by the seller; and

- ensure proper risk management in accordance with Shariah principles.

This reflects the Shariah principle:

“Risk accompanies ownership.”

Since the seller owns the asset before resale, the seller bears the associated risks during that ownership period.

Q2: What is the AAOIFI position regarding takaful cost?

Answer:

According to AAOIFI Shariah Standard No. 8 (Paras 3/2/6–3/2/7):

- the seller is obligated to bear the takaful cost while the asset remains under the seller’s possession; and

- the seller may include the takaful expense as part of the acquisition cost of the asset.

This means the seller initially bears the takaful responsibility because the seller still owns the asset before transferring ownership to the purchaser.

⸻

Q3: What is the BNM position regarding takaful cost?

Answer:

According to the Bank Negara Malaysia (BNM) Policy Document on Murābahah (Para 17.5):

- the purchaser may absorb the takaful cost before entering into the murābahah contract.

This allows:

- greater operational flexibility; and

- cost-sharing arrangements agreed upon between the parties before the sale contract is concluded.

However, the arrangement must be:

- clearly agreed upon; and

- properly documented.

Comparison Notes: AAOIFI vs BNM on Takaful Cost

AAOIFI Position

- Seller bears takaful cost during ownership period.

- Takaful cost may be included in acquisition cost.

- Emphasises ownership-risk principle.

- Seller remains responsible until ownership transfer.

BNM Position

- Purchaser may absorb takaful cost before murābahah contract.

- Allows more operational flexibility.

- Requires proper contractual documentation.

- Commonly applied in Islamic banking practice.

Case Study 1: AAOIFI Approach with Figures

An Islamic bank purchases industrial machinery for a customer under a murābahah arrangement.

Transaction Details

- Purchase price of machinery: RM200,000

- Takaful contribution paid by the bank: RM5,000

- Total acquisition cost borne by the bank: RM205,000

- Bank’s profit margin: RM25,000

- Final murābahah selling price: RM230,000

The bank obtains takaful coverage while the machinery remains under its ownership before reselling it to the customer.

Analysis

- The bank bore the takaful cost because it owned the machinery.

- The takaful contribution was included as part of the acquisition cost.

- The customer was informed that:

- original cost = RM205,000; and

- profit = RM25,000.

- This arrangement complies with AAOIFI standards.

Case Study 2: BNM Approach with Figures

A customer applies for murābahah vehicle financing from an Islamic bank.

Transaction Details

- Purchase price of vehicle: RM100,000

- Takaful contribution: RM3,000

- Customer agrees to bear takaful contribution before murābahah execution.

- Bank’s disclosed acquisition cost: RM100,000

- Bank’s profit margin: RM15,000

- Final murābahah selling price: RM115,000

Before the murābahah contract is concluded, the customer separately agrees to pay the RM3,000 takaful contribution.

Analysis

- The purchaser absorbed the takaful cost before the sale contract.

- The bank’s murābahah cost excluded the takaful amount.

- Proper documentation separated:

- takaful arrangement; and

- murābahah contract.

- This arrangement is permissible under BNM guidelines.

Notes: Important Principles Regarding Takaful in Murābahah

AAOIFI Emphasis

- Ownership risk remains with seller before sale.

- Seller responsible for takaful during ownership period.

- Takaful expense may be included in cost price.

BNM Emphasis

- Purchaser may absorb takaful cost earlier.

- Greater flexibility in banking operations.

- Proper agreement and documentation required.

Common Shariah Principle

The party bearing ownership risk should generally bear the corresponding liabilities and responsibilities associated with the asset until ownership is transferred.

- Published on

Islamic Contract – Bay’ al-Salam: Legality of Salam

Q1: What is the legal basis for the permissibility of salam?

Answer

The legality of the salam contract is established through:

selling something that does not yet exist (bay‘ al-ma‘dūm).

This exception was permitted because of:

Q2: What is the Qur’ānic basis for salam?

Answer

The permissibility of salam is deduced from the following verse of the Qur’ān:

“You who believe, when you contract a debt for a stated term, put it down in writing…”

(Qur’ān, 2:282)

Ibn ‘Abbās explained that:

The verse also emphasises:

Q3: What evidence from the Sunnah supports salam?

Answer

Ibn ‘Abbās reported that:

when the Prophet Muhammad (SAW) migrated to Madinah,

people were engaging in salam transactions involving fruits for:

“Whoever pays money in advance for something should pay it for a specified measure or specified weight for delivery on a specified date.”

(al-Bukhāri, hadith no. 2240)

This hadith establishes several important conditions of salam:

Q4: Why was salam permitted although it involves future goods?

Answer

Normally, Islamic law prohibits:

selling non-existent goods (bay‘ al-ma‘dūm)

because it may lead to:

Q5: What is the role of ijmā‘ in salam?

Answer

Muslim jurists unanimously accepted:

the permissibility of salam.

This scholarly consensus (ijmā‘) developed because:

Case Study 1: Farmer Salam Financing

A rice farmer requires money before planting season.

A trader enters into salam contract with the farmer.

Contract Details

Analysis

✅ Valid salam contract.

Case Study 2: Palm Oil Producer Financing

An Islamic bank finances a palm oil producer using salam.

Contract Details

Analysis

The salam contract:

✅ Permissible salam arrangement.

Important Principle

Salam is permitted because:

Q1: What is the legal basis for the permissibility of salam?

Answer

The legality of the salam contract is established through:

- the Qur’ān;

- the Sunnah; and

- ijmā‘ (consensus of Muslim jurists).

selling something that does not yet exist (bay‘ al-ma‘dūm).

This exception was permitted because of:

- commercial necessity;

- public interest; and

- the needs of farmers and producers.

Q2: What is the Qur’ānic basis for salam?

Answer

The permissibility of salam is deduced from the following verse of the Qur’ān:

“You who believe, when you contract a debt for a stated term, put it down in writing…”

(Qur’ān, 2:282)

Ibn ‘Abbās explained that:

- this verse includes salam transactions because salam creates:

The verse also emphasises:

- proper documentation;

- specified terms;

- contractual certainty.

Q3: What evidence from the Sunnah supports salam?

Answer

Ibn ‘Abbās reported that:

when the Prophet Muhammad (SAW) migrated to Madinah,

people were engaging in salam transactions involving fruits for:

- one year;

- two years;

- or three years.

“Whoever pays money in advance for something should pay it for a specified measure or specified weight for delivery on a specified date.”

(al-Bukhāri, hadith no. 2240)

This hadith establishes several important conditions of salam:

- full advance payment;

- specified quantity;

- specified quality;

- specified delivery date.

Q4: Why was salam permitted although it involves future goods?

Answer

Normally, Islamic law prohibits:

selling non-existent goods (bay‘ al-ma‘dūm)

because it may lead to:

- uncertainty (gharar);

- disputes;

- injustice.

- farmers and producers required advance financing;

- they needed working capital before harvest or production.

- supports economic activity;

- assists agricultural communities;

- provides Shariah-compliant financing.

Q5: What is the role of ijmā‘ in salam?

Answer

Muslim jurists unanimously accepted:

the permissibility of salam.

This scholarly consensus (ijmā‘) developed because:

- salam was widely practised;

- the Prophet (SAW) approved it;

- society had genuine commercial need for it.

- all major schools of Islamic jurisprudence recognise salam as permissible.

Case Study 1: Farmer Salam Financing

A rice farmer requires money before planting season.

A trader enters into salam contract with the farmer.

Contract Details

- Commodity: 20,000 kg of rice

- Salam price: RM100,000

- Payment: fully paid immediately

- Delivery date: 1 December 2028

- seeds;

- fertiliser;

- labour costs.

Analysis

- Full payment made upfront.

- Delivery deferred.

- Commodity clearly specified.

- helps farmer obtain capital;

- complies with salam requirements.

✅ Valid salam contract.

Case Study 2: Palm Oil Producer Financing

An Islamic bank finances a palm oil producer using salam.

Contract Details

- Commodity: 200 tonnes crude palm oil

- Salam price: RM800,000

- Delivery period: 8 months

- pays full price immediately.

- delivers palm oil after production.

Analysis

The salam contract:

- provides immediate liquidity to producer;

- secures future commodity supply for bank.

✅ Permissible salam arrangement.

Important Principle

Salam is permitted because:

- it fulfils genuine commercial needs;

- it assists producers and farmers;

- it facilitates economic activity.

- strict conditions apply to minimise:

- uncertainty (gharar);

- disputes;

- exploitation.

- full upfront payment;

- specified quantity;

- specified quality;

- specified delivery date.

- Published on

Overview of Classification of Contract in Islamic Commercial Law

Contract

Contracts in Islamic commercial law are generally divided into:

Bilateral Contracts

Definition

A bilateral contract is an agreement where both parties have mutual obligations and responsibilities.

Work or Services Contracts

Definition

Contracts involving performance of work or provision of services for compensation.

Commission-based contract

Islamic Contract

Juʿālah (الجعالة)

Definition

A contract where a person receives commission or reward for completing a specific task or service.

Mechanism of Action

Brokerage or reward-based services.

Agency-based contract

Islamic Contract

Wakālah (الوكالة)

Definition

A contract where one party acts on behalf of another party.

Mechanism of Action

Investment agency services.

Safe Custody Contracts

Definition

Contracts involving safekeeping and protection of assets.

Transfer of debt

Islamic Contract

Ḥiwālah (الحوالة)

Definition

Transfer of debt obligation from one party to another.

Mechanism of Action

Remittance transactions.

Security Contracts

Definition

Contracts that provide assurance or security against default.

Guarantee

Islamic Contract

Kafālah (الكفالة)

Definition

A contract where a guarantor guarantees another person’s obligation.

Mechanism of Action

Bank guarantees.

Pledge

Islamic Contract

Rahn (الرهن)

Definition

A contract where an asset is pledged as collateral for debt.

Mechanism of Action

Islamic pawn broking.

Partnership Contracts

Definition

Contracts involving cooperation between parties to conduct business and share profit or loss.

Partnership by reputation

Islamic Contract

Shirkat al-Wujūh (شركة الوجوه)

Definition

A partnership based on reputation or creditworthiness without capital contribution.

Mechanism of Action

Trading partnership based on reputation.

Partnership by work and services

Islamic Contract

Shirkat al-Abdān (شركة الأبدان)

Definition

A partnership where partners contribute labor, expertise, or services instead of capital.

Mechanism of Action

Professional consultancy partnership.

Partnership by capital

Islamic Contract

Shirkat al-Amwāl (شركة الأموال)

Definition

A partnership where all partners contribute capital.

Mechanism of Action

Business joint venture.

Partnership by combining capital and work

Islamic Contract

Muḍārabah (المضاربة)

Definition

A partnership where one party contributes capital and another contributes expertise or management.

Mechanism of Action

Investment financing.

Leasing Contracts

Definition

Contracts transferring right to use an asset for rental payment.

Financial lease

Islamic Contract

Ijārah Muntahiyah bi al-Tamlīk (الإجارة المنتهية بالتمليك)

Definition

A lease where ownership may transfer to lessee at end of contract.

Mechanism of Action

Islamic home financing.

Operating lease

Islamic Contract

Ijārah (الإجارة)

Definition

A lease where ownership remains with lessor permanently.

Mechanism of Action

Vehicle rental.

Sale Contracts

Definition

Contracts involving transfer of ownership for consideration.

Subject Matter of Sale

Currency

Islamic Contract

Bayʿ al-Ṣarf (بيع الصرف)

Definition

A contract involving exchange of currencies or monetary values.

Mechanism of Action

Foreign exchange transactions.

Rights or intangible properties

Islamic Contract

Ḥaqq Mālī (حق مالي)

Definition

Transfer or sale involving intangible rights or non-physical properties.

Mechanism of Action

Intellectual property rights.

Receivable

Islamic Contract

Bayʿ al-Dayn (بيع الدين)

Definition

A contract involving transfer or sale of receivables/debt.

Mechanism of Action

Trade receivable financing.

Tangible asset

Islamic Contract

Bayʿ (البيع)

Definition

A sale involving physical assets with material existence.

Mechanism of Action

Property or machinery sale.

Cost or Profit Classification

Discounted-based sale

Islamic Contract

Waḍīʿah (الوضيعة)

Definition

A sale where seller offers asset below original purchase price.

Mechanism of Action

Discount or clearance sale.

Cost-based sale

Islamic Contract

Tawliyah (التولية)

Definition

A sale where seller transfers asset at original cost without profit.

Mechanism of Action

Friendly transfer sale.

Negotiated sale

Islamic Contract

Musāwamah (المساومة)

Definition

A sale where price is negotiated without disclosure of original cost.

Mechanism of Action

Ordinary market trading.

Cost plus profit

Islamic Contract

Murābaḥah (المرابحة)

Definition

A sale where seller discloses cost and adds known profit margin.

Mechanism of Action

Islamic financing facility.

Time of Payment Classification

Future payment sale

Islamic Contract

Bayʿ Muʾajjal (بيع مؤجل)

Definition

A sale where payment is deferred to a future date.

Mechanism of Action

Installment financing.

Spot payment sale

Islamic Contract

Bayʿ Naqdan (بيع نقداً)

Definition

A sale where payment is made immediately.

Mechanism of Action

Cash purchase.

Time of Delivery of Object

Future delivery sale

Islamic Contract

Bayʿ al-Salam (بيع السلم)

Definition

A sale where delivery occurs at a future date while payment is made upfront.

Mechanism of Action

Agricultural financing.

Spot delivery sale

Islamic Contract

Bayʿ Ḥāl (بيع حال)

Definition

A sale where delivery occurs immediately after agreement.

Mechanism of Action

Retail purchase transaction.

Loan Contracts

Islamic Contract

Qard (القرض)

Definition

A contract involving temporary transfer of money with obligation to repay equivalent amount without interest.

Mechanism of Action

Qard Hasan financing.

Unilateral Contracts

Definition

Contracts formed through declaration or commitment by one party only.

Will

Islamic Contract

Waṣiyyah (الوصية)

Definition

A declaration regarding distribution of property after death.

Mechanism of Action

Islamic estate planning.

Waiver

Islamic Contract

Ibrāʾ (الإبراء)

Definition

Voluntary release or forgiveness of obligation or right.

Mechanism of Action

Debt rebate.

Donation

Islamic Contract

Ṣadaqah (الصدقة)

Definition

Voluntary charitable transfer of wealth without compensation.

Mechanism of Action

Charitable donation.

Gift

Islamic Contract

Hibah (الهبة)

Definition

Voluntary transfer of ownership without consideration.

Mechanism of Action

Gift from bank to depositor.

Contract

Contracts in Islamic commercial law are generally divided into:

- Bilateral Contracts

- Unilateral Contracts

Bilateral Contracts

Definition

A bilateral contract is an agreement where both parties have mutual obligations and responsibilities.

Work or Services Contracts

Definition

Contracts involving performance of work or provision of services for compensation.

Commission-based contract

Islamic Contract

Juʿālah (الجعالة)

Definition

A contract where a person receives commission or reward for completing a specific task or service.

Mechanism of Action

- Client offers reward for completing task.

- Service provider performs work.

- Reward/commission paid upon successful completion.

Brokerage or reward-based services.

Agency-based contract

Islamic Contract

Wakālah (الوكالة)

Definition

A contract where one party acts on behalf of another party.

Mechanism of Action

- Principal appoints agent.

- Agent performs authorized tasks.

- Agent may receive agreed fee.

Investment agency services.

Safe Custody Contracts

Definition

Contracts involving safekeeping and protection of assets.

Transfer of debt

Islamic Contract

Ḥiwālah (الحوالة)

Definition

Transfer of debt obligation from one party to another.

Mechanism of Action

- Original debtor transfers liability.

- New debtor accepts responsibility.

- Creditor claims payment from new debtor.

Remittance transactions.

Security Contracts

Definition

Contracts that provide assurance or security against default.

Guarantee

Islamic Contract

Kafālah (الكفالة)

Definition

A contract where a guarantor guarantees another person’s obligation.

Mechanism of Action

- Guarantor undertakes responsibility.

- Debtor fulfills obligation.

- Guarantor compensates if default occurs.

Bank guarantees.

Pledge

Islamic Contract

Rahn (الرهن)

Definition

A contract where an asset is pledged as collateral for debt.

Mechanism of Action

- Borrower pledges asset.

- Creditor holds collateral.

- Asset may be sold upon default.

Islamic pawn broking.

Partnership Contracts

Definition

Contracts involving cooperation between parties to conduct business and share profit or loss.

Partnership by reputation

Islamic Contract

Shirkat al-Wujūh (شركة الوجوه)

Definition

A partnership based on reputation or creditworthiness without capital contribution.

Mechanism of Action

- Partners obtain goods using reputation.

- Goods sold in market.

- Profit shared according to agreement.

Trading partnership based on reputation.

Partnership by work and services

Islamic Contract

Shirkat al-Abdān (شركة الأبدان)

Definition

A partnership where partners contribute labor, expertise, or services instead of capital.

Mechanism of Action

- Partners jointly provide services.

- Income generated from work.

- Profit shared according to agreement.

Professional consultancy partnership.

Partnership by capital

Islamic Contract

Shirkat al-Amwāl (شركة الأموال)

Definition

A partnership where all partners contribute capital.

Mechanism of Action

- Partners invest capital.

- Business conducted jointly.

- Profit shared according to agreement.

- Loss shared according to capital contribution.

Business joint venture.

Partnership by combining capital and work

Islamic Contract

Muḍārabah (المضاربة)

Definition

A partnership where one party contributes capital and another contributes expertise or management.

Mechanism of Action

- Investor provides funds.

- Entrepreneur manages business.

- Profit shared according to agreed ratio.

- Financial loss borne by investor unless negligence occurs.

Investment financing.

Leasing Contracts

Definition

Contracts transferring right to use an asset for rental payment.

Financial lease

Islamic Contract

Ijārah Muntahiyah bi al-Tamlīk (الإجارة المنتهية بالتمليك)

Definition

A lease where ownership may transfer to lessee at end of contract.

Mechanism of Action

- Lessor purchases asset.

- Asset leased to customer.

- Customer pays rental installments.

- Ownership transferred at maturity if agreed.

Islamic home financing.

Operating lease

Islamic Contract

Ijārah (الإجارة)

Definition

A lease where ownership remains with lessor permanently.

Mechanism of Action

- Asset leased temporarily.

- Customer uses asset.

- Asset returned after lease period.

Vehicle rental.

Sale Contracts

Definition

Contracts involving transfer of ownership for consideration.

Subject Matter of Sale

Currency

Islamic Contract

Bayʿ al-Ṣarf (بيع الصرف)

Definition

A contract involving exchange of currencies or monetary values.

Mechanism of Action

- Two currencies exchanged.

- Exchange rate agreed upon.

- Immediate possession required.

Foreign exchange transactions.

Rights or intangible properties

Islamic Contract

Ḥaqq Mālī (حق مالي)

Definition

Transfer or sale involving intangible rights or non-physical properties.

Mechanism of Action

- Rights legally recognized.

- Rights transferred contractually.

Intellectual property rights.

Receivable

Islamic Contract

Bayʿ al-Dayn (بيع الدين)

Definition

A contract involving transfer or sale of receivables/debt.

Mechanism of Action

- Creditor owns receivable.

- Receivable transferred or settled.

Trade receivable financing.

Tangible asset

Islamic Contract

Bayʿ (البيع)

Definition

A sale involving physical assets with material existence.

Mechanism of Action

- Asset ownership transferred.

- Buyer pays agreed price.

Property or machinery sale.

Cost or Profit Classification

Discounted-based sale

Islamic Contract

Waḍīʿah (الوضيعة)

Definition

A sale where seller offers asset below original purchase price.

Mechanism of Action

- Seller discloses lower sale price.

- Buyer purchases at discounted value.

Discount or clearance sale.

Cost-based sale

Islamic Contract

Tawliyah (التولية)

Definition

A sale where seller transfers asset at original cost without profit.

Mechanism of Action

- Seller discloses actual cost.

- Asset sold at same purchase price.

Friendly transfer sale.

Negotiated sale

Islamic Contract

Musāwamah (المساومة)

Definition

A sale where price is negotiated without disclosure of original cost.

Mechanism of Action

- Buyer and seller negotiate freely.

- Agreed price finalized.

- Ownership transferred.

Ordinary market trading.

Cost plus profit

Islamic Contract

Murābaḥah (المرابحة)

Definition

A sale where seller discloses cost and adds known profit margin.

Mechanism of Action

- Seller purchases asset.

- Cost and profit disclosed.

- Buyer pays agreed price.

Islamic financing facility.

Time of Payment Classification

Future payment sale

Islamic Contract

Bayʿ Muʾajjal (بيع مؤجل)

Definition

A sale where payment is deferred to a future date.

Mechanism of Action

- Asset delivered immediately.

- Payment made later according to agreement.

Installment financing.

Spot payment sale

Islamic Contract

Bayʿ Naqdan (بيع نقداً)

Definition

A sale where payment is made immediately.

Mechanism of Action

- Buyer pays instantly.

- Seller transfers asset immediately.

Cash purchase.

Time of Delivery of Object

Future delivery sale

Islamic Contract

Bayʿ al-Salam (بيع السلم)

Definition

A sale where delivery occurs at a future date while payment is made upfront.

Mechanism of Action

- Buyer pays in advance.

- Seller delivers goods later.

Agricultural financing.

Spot delivery sale

Islamic Contract

Bayʿ Ḥāl (بيع حال)

Definition

A sale where delivery occurs immediately after agreement.

Mechanism of Action

- Contract finalized.

- Goods transferred immediately.

Retail purchase transaction.

Loan Contracts

Islamic Contract

Qard (القرض)

Definition

A contract involving temporary transfer of money with obligation to repay equivalent amount without interest.

Mechanism of Action

- Lender provides money.

- Borrower uses funds temporarily.

- Borrower repays equivalent amount only.

Qard Hasan financing.

Unilateral Contracts

Definition

Contracts formed through declaration or commitment by one party only.

Will

Islamic Contract

Waṣiyyah (الوصية)

Definition

A declaration regarding distribution of property after death.

Mechanism of Action

- Person specifies beneficiaries.

- Will becomes effective after death.

- Assets distributed accordingly.

Islamic estate planning.

Waiver

Islamic Contract

Ibrāʾ (الإبراء)

Definition

Voluntary release or forgiveness of obligation or right.

Mechanism of Action

- Creditor waives obligation.

- Debtor’s liability reduced or removed.

Debt rebate.

Donation

Islamic Contract

Ṣadaqah (الصدقة)

Definition

Voluntary charitable transfer of wealth without compensation.

Mechanism of Action

- Donor gives asset voluntarily.

- Recipient receives ownership.

Charitable donation.

Gift

Islamic Contract

Hibah (الهبة)

Definition

Voluntary transfer of ownership without consideration.

Mechanism of Action

- Donor offers gift.

- Recipient accepts.

- Ownership transfers immediately.

Gift from bank to depositor.

- Published on

Islamic Contract – Bay’ al-Istisnā‘: Legality of Istisnā‘

Q1: What is the legal basis for the permissibility of istisnā‘?

Answer:

According to Muslim jurists, the legality of the istisnā‘ contract is established through various Islamic legal sources, including:

Q2: What evidence from the Sunnah supports the legality of istisnā‘?

Answer:

The legality of istisnā‘ is supported by a narration reported by Nāfi‘:

“Abdullāh ibn ‘Umar reported that Prophet Muhammad (SAW) requested that a ring be manufactured for him.”

(Ahmad, 2001, hadith no. 12360)

This hadith demonstrates that:

Q3: How does ijmā‘ support the legality of istisnā‘?

Answer:

According to Hanafi jurists, istisnā‘ is also legitimised through:

ijmā‘ (consensus of Muslim jurists).

They argue that:

Q4: What is the role of qiyās and istihsān in legitimising istisnā‘?

Answer:

Qiyās (Analogy)

Jurists use analogy to compare istisnā‘ with other recognised sale contracts involving future delivery and specified assets.

Istihsān (Juristic Preference)

Hanafi jurists particularly rely on istihsān because:

Case Study 1: Manufacturing of Custom Furniture

A hotel owner contracts a furniture manufacturer to produce 200 customised chairs.

Contract Details

Case Study 2: Construction of a Commercial Building

A company appoints a contractor to construct a warehouse under an istisnā‘ arrangement.

Contract Details

Notes: Legal Basis of Istisnā‘

Sunnah

Istisnā‘ is permitted because it facilitates:

Q1: What is the legal basis for the permissibility of istisnā‘?

Answer:

According to Muslim jurists, the legality of the istisnā‘ contract is established through various Islamic legal sources, including:

- the Sunnah;

- ijmā‘ (consensus);

- qiyās (analogy); and

- istihsān (juristic preference).

Q2: What evidence from the Sunnah supports the legality of istisnā‘?

Answer:

The legality of istisnā‘ is supported by a narration reported by Nāfi‘:

“Abdullāh ibn ‘Umar reported that Prophet Muhammad (SAW) requested that a ring be manufactured for him.”

(Ahmad, 2001, hadith no. 12360)

This hadith demonstrates that:

- the Prophet (SAW) requested the manufacture of an item according to specifications; and

- the manufactured item was to be produced in the future.

Q3: How does ijmā‘ support the legality of istisnā‘?

Answer:

According to Hanafi jurists, istisnā‘ is also legitimised through:

ijmā‘ (consensus of Muslim jurists).

They argue that:

- people have continuously practised istisnā‘ transactions throughout different periods of Islamic history;

- scholars did not object to this widespread commercial practice.

Q4: What is the role of qiyās and istihsān in legitimising istisnā‘?

Answer:

Qiyās (Analogy)

Jurists use analogy to compare istisnā‘ with other recognised sale contracts involving future delivery and specified assets.

Istihsān (Juristic Preference)

Hanafi jurists particularly rely on istihsān because:

- strict analogy may initially disallow selling something not yet in existence;

- however, commercial necessity and public interest justify allowing istisnā‘.

- manufacturing;

- construction; and

- economic activities essential for society.

Case Study 1: Manufacturing of Custom Furniture

A hotel owner contracts a furniture manufacturer to produce 200 customised chairs.

Contract Details

- Total contract price: RM80,000

- Manufacturing period: 4 months

- Specifications:

- wood type;

- dimensions;

- colour;

- design.

- The chairs do not yet exist at the time of contract.

- The manufacturer agrees to produce them according to specifications.

- The transaction reflects the essence of istisnā‘.

- Its permissibility is supported by the Sunnah and customary commercial practice.

Case Study 2: Construction of a Commercial Building

A company appoints a contractor to construct a warehouse under an istisnā‘ arrangement.

Contract Details

- Construction price: RM2,500,000

- Completion period: 24 months

- Payment schedule:

- RM500,000 upfront;

- RM1,000,000 during construction;

- RM1,000,000 upon completion.

- The building will be constructed in the future.

- Specifications and delivery timeline are predetermined.

- Payment arrangement is flexible.

- The contract reflects established customary practice accepted by Muslim jurists.

- Sunnah;

- ijmā‘;

- qiyās; and

- istihsān.

Notes: Legal Basis of Istisnā‘

Sunnah

- Prophet Muhammad (SAW) requested manufactured items.

- Hadith supports permissibility of manufacturing contracts.

- Continuous practice of istisnā‘ accepted by Muslim jurists.

- No significant objection from scholars historically.

- Analogy with other valid commercial contracts.

- Juristic preference based on commercial necessity and public interest.

Istisnā‘ is permitted because it facilitates:

- trade;

- manufacturing;

- infrastructure development; and

- societal economic needs within Shariah principles.

- Published on

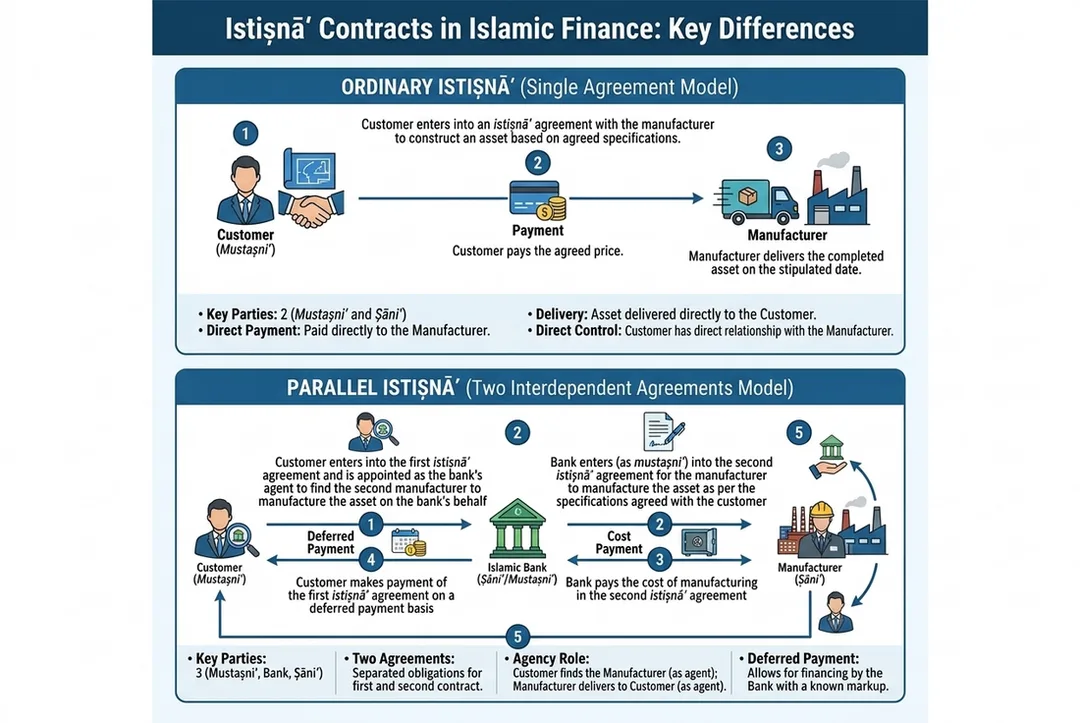

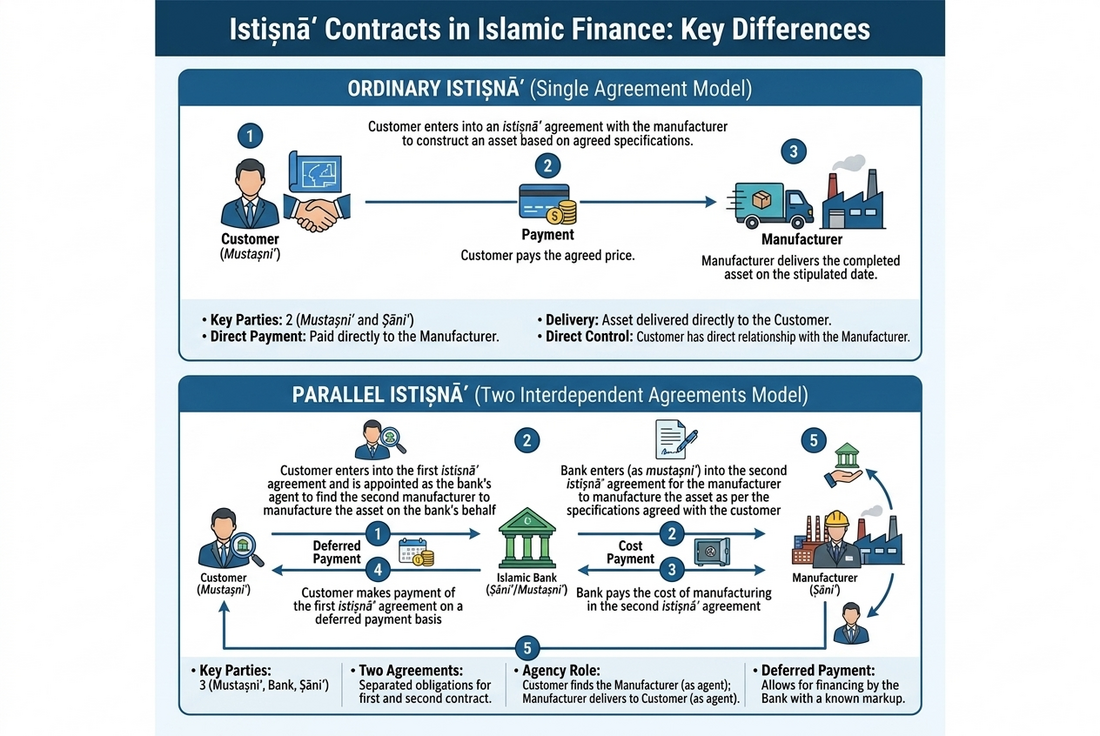

Islamic Contract – Bay’ al-Istisnā‘: Types of Istisnā‘

Q1: What are the types of istisnā‘ contracts?

Answer:

The istisnā‘ contract is generally categorised into two types:

Q2: What is Ordinary Istisnā‘?

Answer:

Ordinary istisnā‘ involves only two contracting parties:

Case Study 1: Ordinary Istisnā‘

A restaurant owner orders customised kitchen equipment from a manufacturer.

Contract Details

Analysis

Q3: What is Parallel Istisnā‘?

Answer:

Parallel istisnā‘ involves:

Case Study 2: Parallel Istisnā‘

An Islamic bank provides financing for the construction of a factory.

First Istisnā‘ ContractBetween:

Second Istisnā‘ Contract (Parallel Istisnā‘)Between:

Analysis

RM5,000,000 - RM4,200,000 = RM800,000

The bank’s profit from the parallel istisnā‘ arrangement is RM800,000.

Notes: Differences Between Ordinary Istisnā‘ and Parallel Istisnā‘Ordinary Istisnā‘

Important Shariah Principle in parallel istisnā‘:

Q1: What are the types of istisnā‘ contracts?

Answer:

The istisnā‘ contract is generally categorised into two types:

- Ordinary Istisnā‘

- Parallel Istisnā‘

Q2: What is Ordinary Istisnā‘?

Answer:

Ordinary istisnā‘ involves only two contracting parties:

- the purchaser (mustaṣni‘); and

- the manufacturer (ṣāni‘).

- the purchaser requests the manufacturer to construct or manufacture an asset according to specified descriptions;

- the parties agree on the contract price;

- payment may be made:

- upfront,

- progressively, or

- on a deferred basis; and

- delivery takes place on an agreed future date.

Case Study 1: Ordinary Istisnā‘

A restaurant owner orders customised kitchen equipment from a manufacturer.

Contract Details

- Asset: Industrial kitchen equipment

- Contract price: RM150,000

- Manufacturing period: 6 months

- Payment arrangement:

- RM50,000 upfront;

- RM50,000 during production;

- RM50,000 upon delivery.

Analysis

- Only two parties are involved:

- purchaser (mustaṣni‘);

- manufacturer (ṣāni‘).

- The manufacturer directly produces the asset.

- Delivery occurs in the future.

Q3: What is Parallel Istisnā‘?

Answer:

Parallel istisnā‘ involves:

- three contracting parties; and

- two separate istisnā‘ contracts.

- the ultimate purchaser (mustaṣni‘); and

- the seller (ṣāni‘).

- the seller agrees to deliver a specifically described asset to the ultimate purchaser.

- the seller (who now becomes the mustaṣni‘); and

- the actual manufacturer (ṣāni‘).

- the seller appoints another party to manufacture or construct the asset.

- the two contracts must remain separate;

- one contract must not be legally contingent upon the other.

Case Study 2: Parallel Istisnā‘

An Islamic bank provides financing for the construction of a factory.

First Istisnā‘ ContractBetween:

- Customer (ultimate purchaser); and

- Islamic bank.

- Factory construction price: RM5,000,000

- Delivery period: 24 months

Second Istisnā‘ Contract (Parallel Istisnā‘)Between:

- Islamic bank; and

- construction company.

- Construction cost payable by bank to contractor: RM4,200,000

- Construction period: 24 months

Analysis

- Two separate contracts exist.

- The customer has no contractual relationship with the contractor.

- The Islamic bank acts as intermediary.

- The bank profits from the difference between:

- selling price to customer = RM5,000,000;

- construction cost = RM4,200,000.

RM5,000,000 - RM4,200,000 = RM800,000

The bank’s profit from the parallel istisnā‘ arrangement is RM800,000.

Notes: Differences Between Ordinary Istisnā‘ and Parallel Istisnā‘Ordinary Istisnā‘

- Involves only two parties.

- Purchaser directly contracts with manufacturer.

- Single istisnā‘ contract.

- Manufacturer personally produces the asset.

- Involves three parties.

- Consists of two separate istisnā‘ contracts.

- Seller may subcontract manufacturing to another party.

- Commonly used in Islamic banking and project financing.

- Contracts must remain legally independent.

Important Shariah Principle in parallel istisnā‘:

- each contract must stand independently;

- performance of one contract cannot be made legally conditional upon the other;

- this preserves contractual certainty and Shariah compliance.